MATRIMONIAL PROPERTY- DIVORCE AND SEPARATION

Contact Us for a Free Consultation Regarding Property Division.

Divorce and Division of Property

When two people enter into a marriage, each spouse is entitled to one-half of all the property acquired during the marriage that still exists at the date of separation. The date of separation is also called “the valuation date” because that is the date used to determine the value of all of the existing assets at the dissolution of the marriage. In a divorce proceeding, one will have to complete a Form 13.1: Financial Statement (Property and Support Claims).

Filling out a Form 13.1 Financial Statement (Property and Support Claims) that involves property issues contains nuances that requires legal expertise. Often times, the value of various assets such as land, vehicles, pension plans, and certain financial investments are not easily calculated.

Call us today if you need advice on calculating the value of your assets on the date of separation.

Separation Agreement:

This can often times make a significant difference in what the final equalization payment would be. One way to go through a divorce without the stress of court is to have a separation agreement. These agreements are enforceable documents and requires both parties to have legal advice.

In some cases, couples may choose to enter into a separation agreement instead of applying for a divorce. A separation agreement is a contract between the couple that outlines the details of their separation. It should include information about how property and debts will be divided, and if there will be any spousal support paid. It can also include information about custody and access of any children of the marriage.

Net Family Property (NFP):

It is necessary to calculate the value of the net family property, which is all the property and assets acquired during the course of the marriage. Property acquired before the marriage will not go towards the net family property unless it is a matrimonial home.

On the date of separation, the home that both parties reside in is classified as the matrimonial home. Regardless of who owned the home before the marriage, the matrimonial home is divided equally between the spouses. These rules do not apply to common-law spouses. Essentially the decision to marry is a decision to enter into a property regime that is set out by the legislation. However, if people do not marry, they are not agreeing to enter into the property regime set out by the legislation.

In order to calculate net family property we will have to look at the assets of each spouse as well as their liabilities on the date of the marriage and the date of separation. If the liability is decreased during the course of the marriage that counts as an asset for the person whose liability has decreased, and the value of the decease of the debt will have to be included in the net family property calculation.

Calculating Net Family Profit (NFP)- A Hypothetical Situation

So, for example, to take a very simplified hypothetical situation, consider the following. The husband owns an investment account valued at $100,000.00, a bank account valued at $10,000.00, and a car valued at $12,000.00 all in his name, at the date of separation. On the date of marriage, he owned none of these things and in fact had a debt of $50,000.00. On the date of marriage, the wife had an investment account valued at $20,000.00, a car valued at $10,000.00, and a personal bank account with $2,000.00, she had no debts.

On the date of separation, the wife’s investment account is $150,000.00, her car which is the same car as at the date of marriage, is valued at $3,000.00 and her personal bank account has $8,000.00. The parties also own a matrimonial home valued at $1,200,000.00. In this hypothetical scenario one would have to calculate each spouse’s net family property. For the husband, his Net Family Profit (NFP) at the date of separation would be all of his assets, as well as an additional $50,000.00.

By paying the debt during the course of the marriage that debt is classified as an asset on the valuation date, representing the gain in the family property. Furthermore, the matrimonial home in the Net Family Profit (NFP) calculation would have to be accounted for in both parties’ NFP.

So the total NFP of the husband is the sum of all of his assets, as well as the value of the debts he has paid during the course of the marriage, and half of the value of the matrimonial home. So to add it all up, his investment account valued at $100,000.00, his bank account valued at $10,000.00, and his car valued at $12,000.00, along with the value of the debt that he has paid off, $50,000.00 and half the value of the matrimonial home, $600,000.00 gives the total value at the date of separation at $772,000.00 and the value of his family property at the date of separation is negative $50,000.00 (because that is a debt).

So the total net family property would be the value of the property at the date of separation minus the total of the debts and liabilities on the date of separation, and from this number you would deduct the value of the assets owned at the date of marriage and you would add the value of the liabilities at the date of marriage.

Applying this to the husband’s situation, his net family property would be $772,000.00 plus (-$50,000.00) for a total net family property of $722,000.00. For the wife, her net family property would be the value of all of the assets minus the debts and liabilities on the date of separation, and from this one would also deduct the value of the assets and add the value of the liabilities on the date of marriage.

The wife would have $600,000.00 from the matrimonial home, and we will add to this the value of the assets on the date of separation which is an investment account valued at $150,000.00, her car which is the same car as at the date of marriage, which is valued at $3,000.00 and her personal bank account which has $8,000.00. The total of all of her assets on the date of separation is $761,000.00. From this we would subtract her assets on the date of marriage and add her liabilities on the date of marriage.

The total value of the assets on the date of marriage includes an investment account valued at $20,000.00, a car valued at $10,000.00, and a personal bank account with $2,000.00, for a total of $32,000.00 and she had no debts. So her net family property would be $761,000.00 minus $32,000.00 which would equal $729,000.00. To calculate the equalization payment one would have to take the higher net family property of the wife and deduct the net family property of the husband. The wife would have to pay one half of the difference between their net family property. So, the wife’s net family property is $761,000.00 and the husband’s net family property is $722,000.00, the difference is $39,000.00, the wife would have to pay half of this amount to the husband.

Her equalization payment would be one half of $39,000.00 which is $19,500.00. Once this amount is paid, both the husband and wife would have equal net family property, the husband would have $722,000.00 plus $19,500.00 for a total of $741,500.00. The wife would have $761,000.00 minus $19,500.00 for a total of $741,500.00.

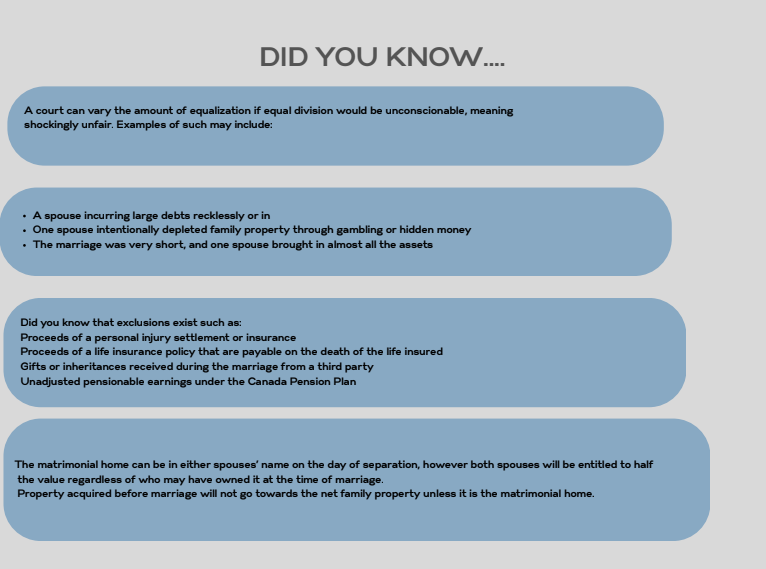

As one can see, this net family property and equalization calculation can become quite complex when many assets are involved or when the valuation of the asset is problematic, such as valuing a pension or a business. There are also other deductions available such as gifts or inheritances acquired after the marriage date, income from gifts or inheritances if the donor specifically states it is to be excluded from the net family property calculation.

Other exclusions include damages from personal injury situations such as car accidents, proceeds from life insurance policies, property excluded by way of a domestic/prenuptial agreement and any property other than the matrimonial home that can be traced back to one of the above excluded types of property.

Exceptions:

The concept of tracing is rarely used, however it does come up in situations where one party intentionally depletes the net family property, so for example, if the husband receives a gift and puts the value of the gift into a car that car would be excluded from the net family property to the extent of the value of the gift. Another example of tracing is if one party sells an asset for under fair market value in a non-arm’s length transaction, than the value can be traced to that asset and the court can set aside that transaction as a fraudulent conveyance.

Conclusion:

The matrimonial home is treated in a very special way in comparison to any other asset type. So, if one of the excluded types of property, such as from an inheritance, is reinvested into a matrimonial home that actually cannot be traced. Any money put into a matrimonial home, no matter from what source, will not be allowed to be deducted. The matrimonial home can be in either spouses’ name at the date of separation, however both spouses will be entitled to half the value of the matrimonial home.

Consider the hypothetical situation above. What if the husband had bought the matrimonial home prior to the marriage? Would that change the equalization payment? It depends on various factors and in certain situations the Court can order unequal division of property. Matrimonial property division can be very complex and small differences in the net family property calculation can lead to significantly varying results.

Under the Ontario Family Law Act, the matrimonial home is a special type of property that is divided differently from other property. This is because the matrimonial home is considered to be the home of both spouses, and is the place where the family lives.

The Family Law Act states that both spouses have an equal right to live in the matrimonial home, regardless of who is the legal owner of the property. This means that if one spouse wants to remain living in the matrimonial home after the marriage has ended, they can do so. The other spouse may be entitled to compensation for their share of the equity in the home.

That is why it is always important to have a family lawyer assisting you through the dissolution of your marriage.